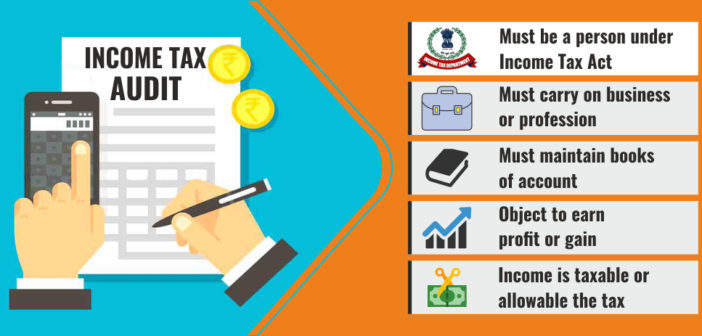

As per the section 44AB of Income Tax Act, the books of accounts for the relevant previous year are required to be audited by a Chartered Accountant and the audit report has to be electronically filed prior to or along with the return of income before the due date. In order to assist to you in complying with these requirements and procedure, your attention is drawn to the following.

|Read Also: Major Changes in Income Tax Law w.e.f 1st April, 2018

1. Taxpayer whose total sales, turnover or gross receipts from business exceeds Rs 1 cr or where Professional receipts

exceed Rs 50 Lakh:

exceed Rs 50 Lakh:

- It is mandatory to fill the Part A of Schedule Profit & Loss A/c and part A of Balance Sheet and also to file the Audit report u/s 44AB of Income Tax Act where the Total Sales, Turnover or Gross Receipts of the business exceeds Rs.1 cr or where Professional receipts exceed Rs 50 Lakh for the Financial Year 2017-18.

- The Audit Report u/s 44AB has to be electronically filed prior to or along with the return of income before the due date.

- The taxpayer has to approve the Audit Report u/s 44AB after it is e-filed by the Chartered Accountant. Without taxpayer approval, the submission of the Audit Report u/s 44AB is NOT COMPLETE.

- For the purpose of all the provisions of Income Tax Act, 1961, the date of approval by the taxpayer will be considered asthe date of filing of the Audit Repor u/s 44AB.

2. Taxpayer reporting Presumptive income under section 44AD:

- As per the provisions of Income Tax Act, the benefit of Section 44AD shall not be applicable where the gross receipts from business exceeds Rs.2 cr in the financial year 2017-18.

- Hence, where the gross receipts/total turnover from the business exceeds Rs.2 cr, it is mandatory to fill the Part A of profit and Loss A/c and Part A of Balance Sheet and also file the Audit Report u/s 44AB of Income Tax Act.

- Taxpayer is advised to follow process as per Sl. No. 1 above strictly in such cases. The benefit of Section 44AD is not available in such cases.

|Read Also: Applicability of Section 234F of Income Tax Act w.e.f. 1st April 2018

3. Taxpayer whose gross receipts in profession exceed Rs 50 Lakhs:

- It is mandatory to fill the Part A of Schedule Profit & Loss A/c and part A of Balance Sheet and also file the Audit report u/s 44AB of Income Tax Act where the gross receipts in profession exceeds Rs 50 Lakhs for the Financial Year 2017-18.

- The audit report has to be electronically filed along with the return of income before the due date.

- The taxpayer is also required to approve/reject the audit report once the same is e-filed by the Chartered Accountant.

- For the purpose of all the provisions of Income Tax Act, 1961, the date of approval by the taxpayer will be considered as the date of filing of the Audit Report.

No.1 Tax Preparation & Filing Company in Tamilnadu

Get Expert Assisted Services at an affordable price

Trusted by 55,000+ Happy Businesses